Fintech SaaS Development

SaaS Development for Fintech Companies & Founders

Fintech products live or die on trust. Open Banking integrations, payments infrastructure, real-time data, and users who expect zero errors with their money. You bring the domain; you get the technical judgment of a CTO and the team to build it, so the product earns that trust the first time.

%20--%3e%3csvg%20version='1.1'%20id='Ebene_1'%20xmlns='http://www.w3.org/2000/svg'%20xmlns:xlink='http://www.w3.org/1999/xlink'%20x='0px'%20y='0px'%20viewBox='0%200%202927.69%20366.04'%20style='enable-background:new%200%200%202927.69%20366.04;'%20xml:space='preserve'%3e%3cstyle%20type='text/css'%3e%20.st0{fill:url(%23SVGID_1_);}%20%3c/style%3e%3clinearGradient%20id='SVGID_1_'%20gradientUnits='userSpaceOnUse'%20x1='25.2367'%20y1='183.1596'%20x2='2902.4714'%20y2='183.1596'%3e%3cstop%20offset='0'%20style='stop-color:%232D363C'/%3e%3cstop%20offset='1'%20style='stop-color:%232D363C'/%3e%3c/linearGradient%3e%3cpath%20class='st0'%20d='M786.72,43.23L667.1,311.61h63.64l23.77-57.51h124.61l23.77,57.51c3.24,7.64,14.41,16.07,36.81,16.07%20s28.37-16.07,28.37-16.07l-120-268.38H786.72z%20M774.45,206.95l42.56-102.75l42.56,102.75H774.45z%20M433.97,199.66h124.6v-48.31%20h-124.6V93.07h141.09V43.23c0,0-151.25,0-163.49,0s-21.72-0.02-30.5,8.77c-8.79,8.79-8.83,17.89-8.83,30.42s0,229.2,0,229.2h207.81%20v-49.84H433.97V199.66z%20M257.97,140.62c0-60.19-44.86-97.39-116.56-97.39H25.24v268.38h62.11v-74.77h54.06h3.07l51.76,74.77%20c17.22,22.3,61.41,18.5,66.71,0l-60.19-86.27C237.64,210.4,257.97,180.87,257.97,140.62z%20M137.96,187.39H87.35V93.84h50.61%20c37.96,0,57.13,17.25,57.13,46.78C195.08,169.75,175.92,187.39,137.96,187.39z%20M1165.16,91.54c26.84,0,49.46,10.74,67.48,31.44%20l11.04-10.19l28.84-26.62c-25.3-30.68-64.03-47.54-110.42-47.54c-83.58,0-145.69,57.89-145.69,138.79%20c0,80.9,62.11,138.79,145.31,138.79c46.78,0,85.5-16.87,110.81-47.92l-39.88-36.81c-18.02,21.09-40.64,31.82-67.48,31.82%20c-50.23,0-85.88-35.27-85.88-85.88C1079.28,126.81,1114.93,91.54,1165.16,91.54z%20M1559.32,149.05h-121.92V43.23c0,0-6.65,0-22.83,0%20c-14.8,0-21.87-0.01-30.58,8.7c-8.71,8.71-8.7,15.76-8.7,30.48c0,17.16,0,229.2,0,229.2h62.11V201.58h121.92v110.03h62.11V43.23%20l-62.12-0.02L1559.32,149.05z%20M2754.47,43.23c0,0-68.85,0-82.65,0c-12.45,0-20.09-0.29-30.32,8.64c-8.48,7.4-8.95,20.05-8.95,30.6%20c0,10.55,0,229.14,0,229.14h121.92c87.8,0,148-52.91,148-134.19C2902.47,96.14,2842.27,43.23,2754.47,43.23z%20M2751.41,260.62h-56.74%20V94.23h56.74c53.29,0,88.18,31.82,88.18,83.2C2839.59,228.8,2804.69,260.62,2751.41,260.62z%20M2517.12,140.46%20c0-60.19-44.86-97.39-116.56-97.39h-116.17v268.38h62.11v-74.77h54.06h3.07l51.76,74.77c17.22,22.3,61.41,18.5,66.71,0l-60.19-86.27%20C2496.8,210.24,2517.12,180.72,2517.12,140.46z%20M2397.11,187.23h-50.61V93.68h50.61c37.96,0,57.13,17.25,57.13,46.78%20C2454.24,169.59,2435.07,187.23,2397.11,187.23z%20M1939.68,172.06c21.86-11.5,35.67-32.21,35.67-59.05%20c0-41.79-34.51-69.78-101.6-69.78h-131.13v268.38h138.79c70.55,0,107.35-26.84,107.35-73.23%20C1988.75,204.65,1969.59,181.64,1939.68,172.06z%20M1804.35,90.01h61.72c30.29,0,46.78,10.35,46.78,31.44%20c0,21.09-16.49,31.82-46.78,31.82h-61.72V90.01z%20M1876.81,264.84h-72.46v-66.33h72.46c32.21,0,49.46,10.74,49.46,33.35%20C1926.27,254.87,1909.01,264.84,1876.81,264.84z%20M2109.87,51.98c-8.79,8.79-8.75,15.93-8.75,30.43c0,14.49,0,229.2,0,229.2h62.11%20V43.23c0,0-11.82,0-22.91,0S2118.66,43.19,2109.87,51.98z'/%3e%3c/svg%3e)

'%3e%3cpath%20id='Path_1'%20data-name='Path%201'%20d='M272.1,36.2H256V67.8c0,10.3,11,19.1,24.6,19.1s25.5-8.9,25.5-19.1V36.2H290V64.7a8.959,8.959,0,0,1-17.9-.1ZM16.7,18.8V84.4H0V5.3H30.1A23.731,23.731,0,0,1,53.9,28.8,23.24,23.24,0,0,1,35.8,51.4L59,84.4H39.1L22.4,58.5V39.6h3.9c6.2,0,11.2-4.6,11.2-10.3A10.655,10.655,0,0,0,26.6,18.8ZM170.4,84.4V1.5H154.6V40.6A21.839,21.839,0,0,0,139,34.2c-13,0-23.6,11.5-23.6,25.8,0,14.2,10.6,25.8,23.6,25.8,6.2,0,12-2.4,15.6-6.8v5.4ZM143.5,72.3c-6.4,0-11.6-5.7-11.6-12.7s5.2-12.7,11.6-12.7,11.6,5.7,11.6,12.7c-.1,7-5.3,12.7-11.6,12.7m93.3-30.9a20.956,20.956,0,0,0,7-15.3,20.744,20.744,0,0,0-5.7-14.2c-3.8-4.1-10.4-6.6-19.4-6.6H191.8V84.4h34.8c13.3-.2,24.1-10.3,24.1-22.7-.1-9-3.3-15.4-13.9-20.3M223.4,70.7H208.3V19.5h10.6a8.3,8.3,0,0,1,8.5,8.2,8.557,8.557,0,0,1-8.5,8.5h-5.6V50.5h10.3a9.907,9.907,0,0,1,9.8,10.2c-.2,5.6-3.9,9.7-10,10'%20fill='%232d363c'/%3e%3cpath%20id='Path_2'%20data-name='Path%202'%20d='M73,54.1a9.6,9.6,0,0,1,19.2,0Zm34.8,9c.1-1.1.2-2.2.2-3.3.2-17.1-11-26.4-25.4-26.4a26.4,26.4,0,0,0,0,52.8c11,0,19.6-5,24-12.8L93.8,67.5a10.762,10.762,0,0,1-9.9,6A10.546,10.546,0,0,1,73.1,63.1ZM313.5,1.5h15.8V84.4H313.5Zm26.9,0h15.8V84.4H340.4Z'%20fill='%232d363c'/%3e%3c/g%3e%3c/svg%3e)

'%3e%3cpath%20id='Path_9755'%20data-name='Path%209755'%20d='M136.278,137.525a.942.942,0,0,0-.967-.925h-1.345a.942.942,0,0,0-.967.925l.042,14.582a.906.906,0,0,0,.925.925h1.345a.942.942,0,0,0,.967-.925V137.525Z'%20transform='translate(-76.115%20-78.181)'%20fill='%23293338'%20fill-rule='evenodd'/%3e%3cpath%20id='Path_9756'%20data-name='Path%209756'%20d='M144.9,137.683v.672a.508.508,0,0,0,.546.546h9.582a.827.827,0,0,0,.8-.8v-1.219c0-.42-.378-.883-.8-.8,0,0-9.245.925-9.582.967a.578.578,0,0,0-.546.63Z'%20transform='translate(-83.014%20-77.877)'%20fill='%23293338'%20fill-rule='evenodd'/%3e%3cpath%20id='Path_9757'%20data-name='Path%209757'%20d='M119.153,153.032a3.742,3.742,0,0,1-3.866-3.824v-5.8h-.714a.723.723,0,0,1-.672-.672v-.967a.691.691,0,0,1,.672-.672h.714v-3.572a.906.906,0,0,1,.925-.925h1.345a.9.9,0,0,1,.883.925V141.1h2.1a.64.64,0,0,1,.672.672v.967a.663.663,0,0,1-.672.672h-2.1v5.379a1.7,1.7,0,0,0,1.807,1.807h.21a.683.683,0,0,1,.714.714v1.051a.736.736,0,0,1-.714.714h-1.3Z'%20transform='translate(-65.042%20-78.181)'%20fill='%23293338'%20fill-rule='evenodd'/%3e%3cpath%20id='Path_9758'%20data-name='Path%209758'%20d='M71.019,152.52c0-3.11-1.849-6.22-6.052-6.22C61.1,146.3,59,149.326,59,152.52c0,3.362,2.269,6.346,6.052,6.346,2.563,0,5.043-1.3,5.547-3.53.042-.252-.168-.714-.546-.714H68.2a.883.883,0,0,0-.756.42,2.719,2.719,0,0,1-2.4,1.135,2.786,2.786,0,0,1-2.816-2.648H70.01a.909.909,0,0,0,1.009-1.009Zm-8.741-1.3a2.7,2.7,0,0,1,2.732-2.4,2.787,2.787,0,0,1,2.816,2.4Z'%20transform='translate(-33.213%20-83.805)'%20fill='%23293338'%20fill-rule='evenodd'/%3e%3cpath%20id='Path_9759'%20data-name='Path%209759'%20d='M155.119,152.52c0-3.11-1.849-6.22-6.052-6.22-3.866,0-5.967,3.026-5.967,6.22,0,3.362,2.269,6.346,6.052,6.346,2.563,0,5.043-1.3,5.547-3.53.042-.252-.168-.714-.546-.714H152.3a.883.883,0,0,0-.756.42,2.747,2.747,0,0,1-2.437,1.135,2.805,2.805,0,0,1-2.774-2.648h7.775a.909.909,0,0,0,1.009-1.009Zm-8.741-1.3a2.779,2.779,0,0,1,5.505,0Z'%20transform='translate(-81.971%20-83.805)'%20fill='%23293338'%20fill-rule='evenodd'/%3e%3cpath%20id='Path_9760'%20data-name='Path%209760'%20d='M60.561,136.594H35.431a1.067,1.067,0,0,0-1.051,1.051l.042,9.876s-5.379-9.792-5.673-10.3a1.838,1.838,0,0,0-1.639-.925H25.051A1.067,1.067,0,0,0,24,137.351v14.456a1.015,1.015,0,0,0,1.051,1.051h1.3a1.015,1.015,0,0,0,1.051-1.051l-.042-10.128s5.421,9.834,5.715,10.212a1.652,1.652,0,0,0,1.6.925h1.933a1.015,1.015,0,0,0,1.051-1.051V138.99h22.9a.736.736,0,0,0,.714-.714v-1.051a.729.729,0,0,0-.714-.63Z'%20transform='translate(-12.922%20-78.007)'%20fill='%23293338'%20fill-rule='evenodd'/%3e%3cpath%20id='Path_9761'%20data-name='Path%209761'%20d='M94,148.7a2.266,2.266,0,0,1,2.227,1.093c.126.336.378.378.756.378H98.5a.585.585,0,0,0,.546-.546c0-1.723-2.1-3.32-5.043-3.32-3.026,0-5.043,1.471-5.043,3.74,0,1.807,1.429,2.816,3.11,3.32.8.168,2.185.5,2.816.714.672.168,1.3.378,1.3.967,0,.967-.967,1.261-2.1,1.261a2.446,2.446,0,0,1-2.353-1.177c-.168-.42-.5-.5-.925-.5H89.288a.632.632,0,0,0-.588.588v.21c0,1.681,2.269,3.446,5.421,3.446,2.185,0,5.3-.925,5.3-3.866,0-1.723-1.135-2.942-3.026-3.446-.714-.168-2.437-.672-2.816-.714-.714-.21-1.345-.42-1.345-.967C92.15,149,92.99,148.7,94,148.7Z'%20transform='translate(-50.432%20-83.805)'%20fill='%23293338'%20fill-rule='evenodd'/%3e%3c/g%3e%3c/svg%3e)

'%3e%3cpath%20id='path13592_1_'%20class='cls-1'%20d='M22.71,659.121a3.638,3.638,0,0,0,2.652-.773,4.9,4.9,0,0,0,1.5-3.558c0-1.663-1.064-1.854-1.463-1.854a2.556,2.556,0,0,0-1.422.574l-1.272,5.611Zm1.6-7.573a4.431,4.431,0,0,1,2.652-.948c1.979,0,3.3,1.48,3.3,3.99a7.05,7.05,0,0,1-1.521,4.348c-1.954,2.394-4.431,2.369-6.526,2.369L21.1,666.03l-.133.1c-.457,0-.89-.025-1.347-.025-.673,0-1.264.042-2,.058l-.1-.141s.7-2.095,1.563-5.695c.906-3.783,1.762-8.205,1.837-9.1l.141-.141,3.375-.549.116.141-.241.873ZM17.165,661.1l-.158.158a12.127,12.127,0,0,1-1.779.216c-1.488,0-3.683-.224-2.752-3.99.623-2.544,1.072-4.448,1.072-4.448l-1.38.042-.116-.158.574-2,.141-.1h1.3l.574-2.552.141-.141c1.48-.332,1.879-.432,3.242-.831l.116.116-.873,3.433,2.012-.042.083.141c-.274.831-.357,1.047-.615,1.979l-.158.141-1.821-.042s-.366,1.538-.89,3.666c-.557,2.311-.266,2.195.291,2.411a2.317,2.317,0,0,0,1.463-.166l.116.1-.582,2.062ZM6.117,652.679c-.931,0-1.979.474-2.585,3.35-.673,3.2.673,3.408,1.322,3.408.59,0,1.854-.324,2.486-3.392.432-2.145.083-3.367-1.222-3.367m4.614,3.367c-.848,4.847-3.866,5.462-6.418,5.462-2.519,0-4.847-1.737-4.182-5.487.515-2.935,2.253-5.645,6.493-5.445,2.951.15,4.689,2.178,4.107,5.47'%20transform='translate(0%20-593.488)'/%3e%3cpath%20id='path13608_1_'%20class='cls-1'%20d='M404.673,635.543l3.059,5.828-.116.158-2.195.058-.158-.116c-.515-1.388-2.743-5.753-2.743-5.753-.574,2.511-.69,3.1-1.189,5.711l-.141.116-2,.042-.083-.116s1.056-4.381,1.97-8.438c.424-1.9,1.089-4.9,1.355-6.717l.141-.116,2.153-.357.116.141c-.4,1.363-2.278,9.469-2.278,9.469,1.413-1.239,3.774-3.716,4.09-4.049l.216-.116h2.27l.058.175c-.565.441-1.6,1.388-1.979,1.721l-2.552,2.361Zm-7.557,5.894-.158.116-2.02.058-.083-.141a63.97,63.97,0,0,0,1.521-7.174c.017-1.189-.732-1.58-1.663-1.58a4.264,4.264,0,0,0-2.627,1.047c-.732,3.317-.973,4.364-1.6,7.665l-.141.116-2.012.058-.1-.141s.6-2.419,1.139-4.938c.424-1.97.773-3.591.931-4.946l.141-.141a19.693,19.693,0,0,0,2.095-.357l.1.141-.274,1.006a5.65,5.65,0,0,1,3.4-1.205,2.518,2.518,0,0,1,2.785,2.569c.008,1.455-1.239,6.459-1.43,7.848m-11.248-8.671c-.3,0-.59-.017-.89-.017a5.436,5.436,0,0,0-3.1.831,5.279,5.279,0,0,0-2.112,4.073,2.3,2.3,0,0,0,2.311,2.469,3.481,3.481,0,0,0,2.369-.973l1.422-6.385Zm1.463,2.511c-.69,3.043-.831,3.8-1.222,6.143l-.141.141-1.854.042-.1-.141.141-.79a4.211,4.211,0,0,1-2.885,1.006,3.591,3.591,0,0,1-3.658-3.891,7.166,7.166,0,0,1,1.58-4.248c1.837-2.153,4.389-2.269,6.21-2.269l2.727.025.1.158-.9,3.824Zm-18.921,4.739a6.749,6.749,0,0,0,4.049-.848,5.171,5.171,0,0,0,2.153-4.032,2.214,2.214,0,0,0-2.353-2.494,4.22,4.22,0,0,0-2.353.831c.008.008-1.372,6.06-1.5,6.543M366,641.462c.133-.6.981-4.115,1.854-8.064.748-3.384,1.264-5.5,1.446-7.083l.158-.141,2.153-.374.1.141-.549,2.195-.914,3.8a5.464,5.464,0,0,1,2.885-.89,3.507,3.507,0,0,1,3.6,3.816,7.077,7.077,0,0,1-1.638,4.431c-1.779,2.037-3.974,2.178-6.526,2.278H367.48l-1.38.017-.1-.125Z'%20transform='translate(-335.558%20-573.776)'/%3e%3cpath%20id='path13616_1_'%20class='cls-1'%20d='M320,165.167a10.263,10.263,0,1,1,10.259,10.267A10.268,10.268,0,0,1,320,165.167'%20transform='translate(-293.383%20-142.023)'/%3e%3cpath%20id='path13620_1_'%20class='cls-1'%20d='M194.718,10.142a5.886,5.886,0,1,1,5.886,5.886h0a5.9,5.9,0,0,1-5.886-5.886h0m-30.318,13A23.143,23.143,0,0,1,187.511,0V8.363a14.777,14.777,0,1,0,14.806,14.748v-.025l8.363.008a23.14,23.14,0,1,1-46.28.05'%20transform='translate(-150.718)'/%3e%3c/g%3e%3c/svg%3e)

$395B

Global fintech market 2025

16%

Annual market growth rate

88%

AI adoption among top-performing fintechs

2019

Running JamDoughnut since

Fintech is a different kind of hard

Financial products don't get the benefit of the doubt. Your users are trusting you with their money, their data, and their financial decisions. One confusing screen or one failed transaction is enough to lose them - permanently.

With a $395B global market growing at 16% annually, the opportunity is clear. But so is the bar: most development agencies can build an app. Far fewer have the judgment to build a fintech product that users actually trust.

Open Banking & third-party integrations

Connecting to banking APIs, transaction data providers, and payment processors requires specialist knowledge - and things break in ways that are hard to predict without experience. Data handling obligations come with every connection.

Payments infrastructure

Card processing, wallets, instant payouts. Each adds compliance obligations and technical complexity that generic agencies routinely underestimate. Getting payments wrong is not a recoverable bug.

Real-time data & reliability

Fintech users expect instant feedback. Delayed transactions, stale balances, or slow dashboards erode trust faster than any bug report. Eventual consistency is not a fintech architecture.

Security & data privacy

Financial data is among the most sensitive there is. Security can't be an afterthought - it has to be designed into every layer from day one. GDPR, PCI-DSS, and FCA requirements aren't optional extras.

Regulatory complexity

FCA, GDPR, PSD2, PCI-DSS - and now the EU AI Act. The compliance landscape in fintech is dense and evolving. A development partner who doesn't know this space can cost you far more than their invoice.

From idea to fintech product - built to be trusted

We've built fintech from scratch - Open Banking integrations, payment wallets, transaction engines, and the mobile apps your users interact with every day. Here's what we bring to your project.

Open Banking integration

We've done it. Transaction monitoring, account linking, and data feeds - connected, reliable, and built to the compliance standards your product requires.

Payments & wallet architecture

Credit card processing, in-app wallets, instant payouts. Designed for reliability and built to scale as your transaction volume grows.

iOS & Android apps

Native mobile applications that match the polish your fintech brand demands - and perform the way your users expect financial software to perform.

Real-time data systems

Dashboards, notifications, and transaction feeds that update instantly. Because in fintech, "eventual consistency" is not good enough for users.

Security-first architecture

Authentication, encryption, audit trails, and data handling designed in - not bolted on. Infrastructure that stands up to regulatory scrutiny and security reviews.

A codebase you own

Clean, documented, and built to scale. Whether you bring on a CTO later or raise a Series A, your technical foundation will hold up.

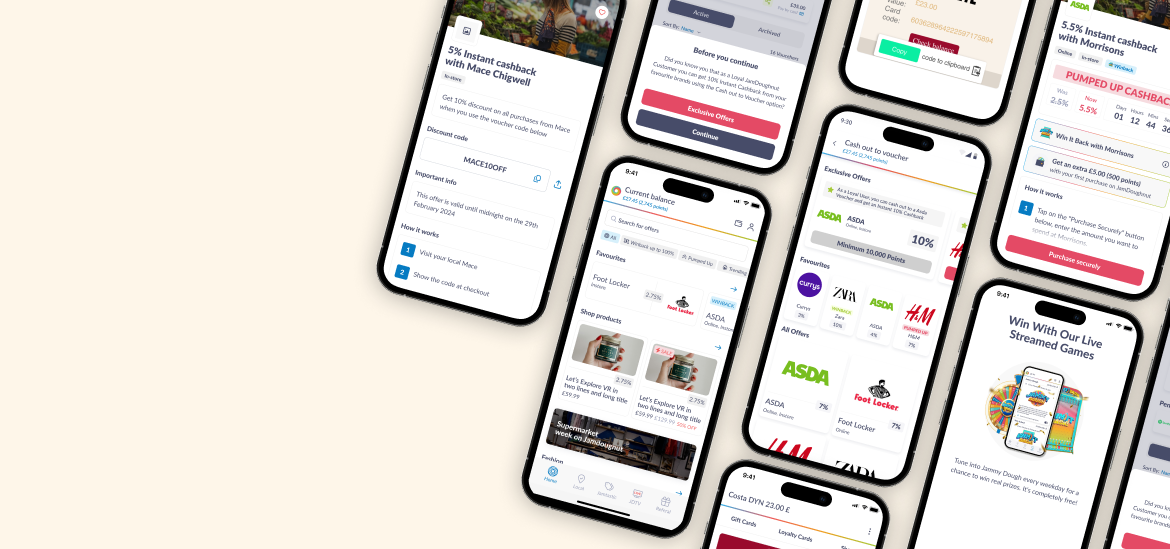

We helped JamDoughnut become the UK's leading cashback platform

JamDoughnut is a UK fintech startup that rewards users with instant cashback on everyday spending - powered by Open Banking. They came to us as a founder with a vision. Over five years later, we're still their dedicated product team.

Project

JamDoughnut

Industry

Fintech / Open Banking / Rewards

Location

United Kingdom

Partnership since

2019 (ongoing)

Services

5-person dedicated product team

What we built

Open Banking integration for real-time transaction monitoring

Instant cashback engine across 100+ brand partnerships

In-app wallet ("JamJar") with credit card payment processing

iOS & Android native applications

Voucher sharing and referral mechanics

Campaign and influencer management tools

Brand partnership management system

The Result

98% of JamDoughnut reviews are 4 or 5 stars. 75% of users acquired through referrals - the product sells itself. 100+ active brand partnerships. Two industry awards. And a partnership that's been running since 2019 because the product keeps growing.

“VeryCreatives has implemented their creative skills to ideate effective concepts and think through possible problems.”

James Walker

Founder, JamDoughnut

AI & Fintech

AI in fintech is a genuine opportunity.

It also has real regulatory teeth.

Unlike MarTech (where AI is table stakes) or generic SaaS (where the stakes of a wrong AI output are low), fintech sits in a different category: 88% of top-performing fintechs are already using AI - but fintech AI touches decisions that directly affect people's money, credit, and access to financial services. That changes everything about how you build it.

The EU AI Act classifies fintech AI as high risk - and the deadline is August 2026

Credit scoring, lending decisions, fraud profiling, and AML risk assessment are all explicitly classified as high-risk AI systems under the EU AI Act. From August 2026, this means: documented training data, explainable outputs, human oversight mechanisms, and full audit trails. The FCA takes a parallel approach under its principles framework - if an AI system influences a decision that affects a customer's financial situation, you need to be able to explain it.

The fintech products getting this right are building explainability and human oversight into the architecture from day one. The ones that aren't are facing either a compliance retrofit or a product rebuild in 2026.

Where AI genuinely belongs in a fintech product

Not every AI use case in fintech carries the same regulatory weight. The products moving fastest are applying AI where the value is high and the compliance burden is manageable - and keeping human judgment firmly in the loop where the stakes are highest.

Fraud detection & transaction monitoring

The clearest win in fintech AI: pattern recognition across transaction data, real-time anomaly flagging, and automated blocking of suspicious activity in under 50 milliseconds. AI here reduces fraud losses by up to 40%. Regulatory risk is relatively manageable - you're detecting suspicious patterns, not making credit decisions.

Personalised financial insights

Spending categorisation, cashback matching, financial health scoring - AI that gives users a clearer picture of their own money. High user value, low regulatory risk, and a natural fit for products built on Open Banking data. This is what JamDoughnut does at its core.

KYC & AML document automation

AI-assisted identity verification, document processing, and sanctions screening - dramatically reducing manual review time without removing the human decision layer. The AI surfaces, the human approves. Regulators are comfortable with this model when it's properly documented.

Credit risk augmentation (not replacement)

AI that surfaces alternative data signals and patterns to assist credit officers - not replace them. 80% of digital loans are now approved instantly via AI, but the products doing this well have an explainability layer built in. Human oversight for edge cases. Full audit trail. This is the architecture that survives a regulator inquiry.

If you're building a fintech product and working out where AI fits - and what it means for your compliance posture - that's exactly the conversation to start in a Product Clarity Sprint.

How the fintech build landscape has changed

Three years ago, building a fintech product from scratch meant dealing with the full regulated banking infrastructure. That's changed significantly - and it changes what's possible for a founder without a banking licence.

Open Banking data APIs (TrueLayer, Yapily, Plaid) have commoditised access to transaction data. Banking-as-a-Service providers (Stripe Treasury, Griffin, Railsr) now handle the regulated layer - accounts, payments, and card issuance - so founders can build the product experience on top of proven infrastructure rather than becoming a regulated entity themselves. This has made it faster and cheaper to build a fintech product than at any point in the industry's history.

The catch: the product layer that sits above BaaS still needs to earn user trust in the way only purpose-built financial software can. The compliance requirements at the product level - data handling, audit trails, FCA rules, and now AI Act obligations - still require specialist architecture. Generic development agencies can plug in Stripe. Very few know what it means to build the financial product experience on top of it well.

Is This Right for You?

Is VeryCreatives right for your fintech build?

We work best with a specific kind of fintech founder. Here's an honest breakdown so you can self-select.

You might be a great fit if…

You're a fintech domain expert, founder, or product owner - but not a developer

You're an established financial company launching a new digital product without pulling your internal team apart

You need Open Banking, payments, or wallet functionality built right the first time

You want a partner who understands fintech compliance, not just code

You want AI built with explainability and compliance architecture, not as a feature flag

You want one team handling strategy, design, and development

You're building for long-term trust and growth, not just an MVP checkbox

We're probably not the right fit if…

You already have a technical co-founder managing development and just need extra resource

You need a fully regulated banking infrastructure built in-house from scratch - we work on the product layer above BaaS

You're looking for the cheapest quote, not the best outcome

How It Works

From first call to live fintech product - here's the process

Four stages. One partner. No handoffs between strategy, design, and development teams.

1

Product Clarity Sprint - Weeks 1-2

A focused, paid sprint that turns your idea into a clear product plan: Scope, integrations, compliance touchpoints, BaaS vs build decisions, AI strategy, and a budget you can understand. No vague estimates.

2

Design

We design every screen, every interaction. In fintech, trust is built through clarity - so we put extra care into flows that handle money, permissions, and sensitive data. Users need to understand exactly what they're authorising.

3

Build

A dedicated team of our developers and designers builds, led by a Product Delivery Lead who reports to you weekly. You stay focused on your business - not on debugging integrations or decoding API documentation. Full staging environment access, and a clean codebase you own.

4

Beyond Launch

Whether you need light maintenance or a dedicated Team-as-a-Service, we stay with you. JamDoughnut has been with us since 2019. Most of our clients are long-term partners, not one-off projects.

Common questions about fintech SaaS development

Why VeryCreatives?

Ready to build your fintech product?

You understand the financial domain.

We handle the product, design, and development - including the hard parts like Open Banking, payments infrastructure, and AI that holds up to regulatory scrutiny. Together, we build something your users will trust.

Our founders Máté and Ferenc take every first call personally.

Usual response time: 48 hours.

Contact Us

We work with about 12 founders per year. If you're a non-technical founder with a SaaS idea and a defined budget, the next step is a 30-minute free discovery call. We'll talk through your idea, your stage, and whether we're the right partner for what you're trying to build. If we're not, we'll tell you who is.

What is going to happen?

Our Account Manager colleagues will contact you to schedule an online consultation with our founders, Máté and Ferenc. In this (free of charge) consultation, they will discuss your idea and provide expert feedback on product development.

Your data is safe

Don't worry, we won't use the information you provide here for anything we wouldn't want you to do.

What time zone are you in?

We are based in Budapest, Hungary and our time zone is GMT+2. This gives us the flexibility to serve both EU and middle-eastern clients.

Or would you instead write an email?

Feel free to write to hello@verycreatives.com! We usually reply by the next working day at the latest.